Institutional Insights: Goldman Sachs SP500 Positioning & Key Levels 13/05/25

.jpeg)

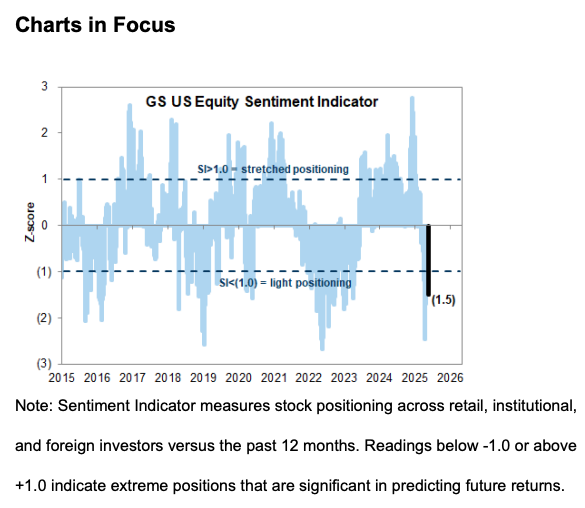

Equity Positioning and Key Levels

FICC and Equities | 12 May 2025 |

Below is a recap of the GS positioning metrics:

Summary:

1. CTA Corner: The systematic macro community has slightly increased their positions but remains below average. Their positioning has improved from 1 out of 10 three weeks ago to nearly 3.5, equivalent to $185 billion in global equities. We anticipate continued buying, although at a slower pace, decreasing from $59 billion last week to $32 billion next week. Of this, $13 billion (41%) is expected to be in US equities.

2. GS PB: From May 2 to May 8, the GS Equity Fundamental L/S Performance Estimate increased by 0.72%, compared to MSCI World TR's 1.25% gain. This was driven by a beta of +0.88%, offset by an alpha of -0.16% due to short side losses. Meanwhile, the GS Equity Systematic L/S Performance Estimate decreased by 0.08% in the same period, affected by negative alpha from short side losses, with beta remaining flat.

3. Buybacks: Weekly flows have remained consistent, finishing at 1.1 times the 2024 YTD average daily trading volume (ADTV) and 1.6 times the 2023 YTD ADTV, with a focus on Financials, Consumer Staples, and Health Care sectors.

CTA Corner Details:

- CTA Flows for the next week:

- Flat market: $21.49 billion in purchases ($7.61 billion into the US)

- Rising market: $26.06 billion in purchases ($12.32 billion into the US)

- Falling market: $0.12 billion in purchases ($1.05 billion out of the US)

- CTA Flows for the next month:

- Flat market: $23.11 billion in purchases ($13.46 billion into the US)

- Rising market: $49.65 billion in purchases ($31.56 billion into the US)

- Falling market: $78.73 billion in sales ($11.92 billion out of the US)

- Key SPX Pivot Levels:

- Short-term: 5584

- Medium-term: 5742

- Long-term: 5492

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!