SP500 LDN TRADING UPDATE 19/3/26

SP500 LDN TRADING UPDATE 19/3/26

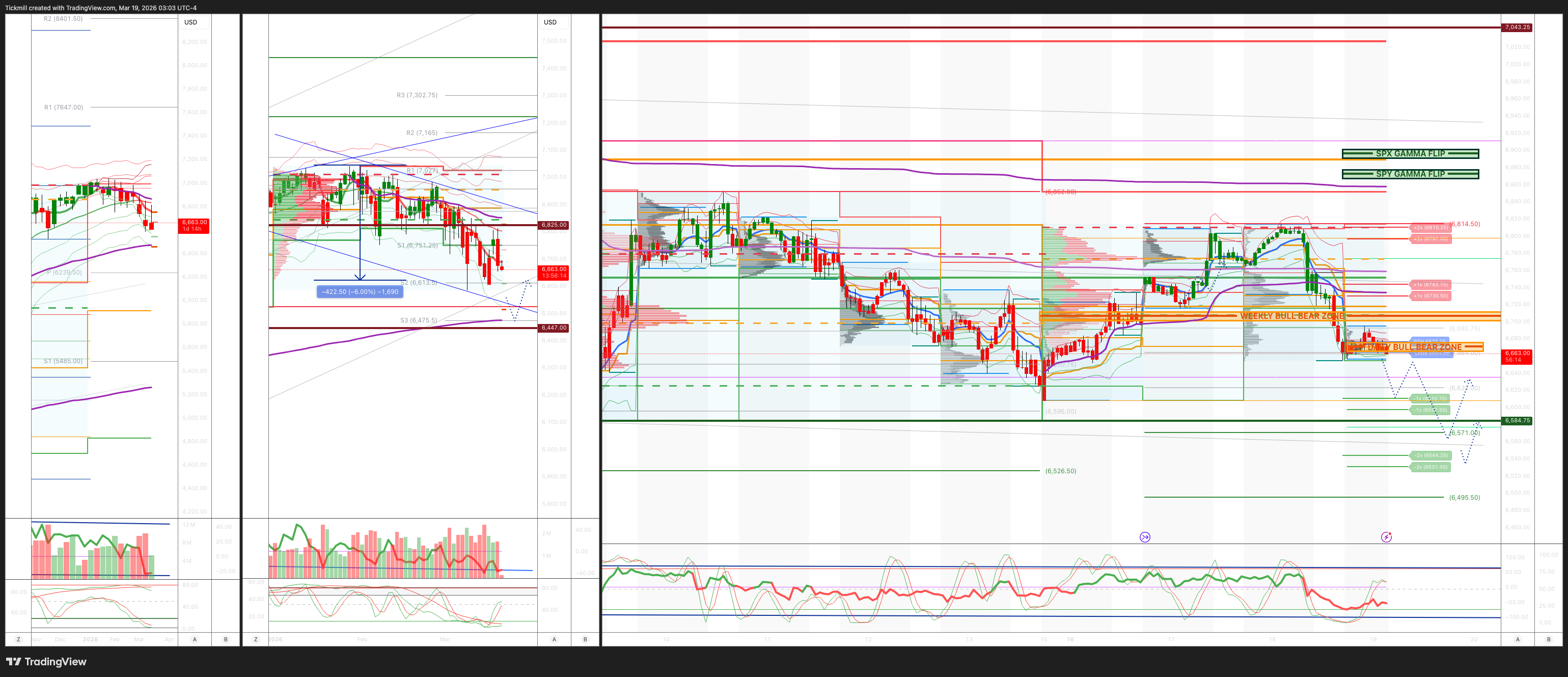

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6700/10

WEEKLY RANGE RES 6825 SUP 6426

Weekly Straddle Range: 199 -point straddle implies a weekly range of [6426, 6824]; monitor 1.5x and 2x moves for key reactions.

March OPEX Straddle: 232.8-point range suggests OPEX-to-OPEX movement between [6677, 7142].

March QOPEX Straddle: 368.55-point range projects [6466, 7203], based on December OPEX.

March EOM Straddle: 255.4-point straddle indicates a monthly range of [6623, 7101]. .

DEC2025 to DEC2026 OPEX straddle spans 945 points, outlining a range of [5889, 7779]."

DAILY VWAP BEARISH 6691

WEEKLY VWAP BEARISH 6777

MONTHLY VWAP BEARISH 6869

DAILY STRUCTURE – BALANCE - 6818/6627

WEEKLY STRUCTURE – OTFD - 6852

MONTHLY STRUCTURE - OTFD

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFD): This describ@es a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6667/54

GAMMA FLIP 6875

DAILY RANGE RES 6743 SUP 6610

2 SIGMA RES 6810 SUP 6544

VIX BULL BEAR ZONE 22

PUT/CALL RATIO 1.3 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

TRADES & TARGETS

SHORT ON ACCEPTANCE BELOW 6650 TARGET DAILY RANGE SUP

LONG ON REJECT/RECLAIM DAILY RANGE SUP TARGET 6650

LONG ON REJECT/RECLAIM 6560/70 TARGET6630

LONG ON REJECT/RECLAIM 6526/36 TARGET6584

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Lower’

S&P closed down 136bps at 6,624 with a Market-On-Close (MOC) imbalance of $1.4bn to buy. The Nasdaq 100 (NDX) dropped 143bps to 24,425, the Russell 2000 (R2K) fell 164bps to 2,479, and the Dow Jones declined 163bps to 46,225. Total trading volume across all U.S. equity exchanges was 19.42 billion shares, slightly below the year-to-date daily average of 19.53 billion. The VIX rose 11.31% to 24.9, WTI Crude surged 250bps to $99.67, the U.S. 10-year yield increased 7bps to 4.27%, gold dropped 326bps to $4,842, the dollar index (DXY) gained 60bps to 100.17, and Bitcoin tumbled 515bps to $70,695.

Market sentiment remained cautious as institutional investors stayed on the sidelines ahead of the Federal Reserve's announcements and ongoing geopolitical tensions. Crude oil, volatility, the U.S. dollar, and bond yields all moved higher. QatarEnergy reported missile attacks on Ras Laffan Industrial City, the world’s largest LNG facility, causing significant damage and fires, though no casualties were reported.

Economic data showed a hotter-than-expected Producer Price Index (PPI), but PCE-relevant components came in slightly below expectations. As anticipated, the Federal Reserve left the fed funds rate unchanged, with Chair Jerome Powell delivering hawkish commentary during the press conference. Powell emphasized, “If we don’t see progress on inflation, you won’t see that rate cut,” and noted that the median projection for the federal funds rate is 3.4% by year-end.

In financials, price action was mixed and highly sensitive to headlines. Alternative assets and banks gained on inflation fears as hedges came off, but reflation winners faced pressure. Short interest in financials had seen the largest increase among all sectors over the past month. Fintech and "buy now, pay later" names underperformed following reports of private credit investors pulling back from consumer loans. Payments companies like Visa (V) and Mastercard (MA) also faced pressure after news of a Stripe-backed crypto startup introducing an AI payments protocol. Regulatory announcements are expected tomorrow, including discussions on Basel III endgame, broader risk-based capital changes, and GSIB surcharge proposals.

Post-market earnings highlights included Micron (MU), which initially rose 2% but ended flat (+1%). Despite a strong beat and elevated guidance (Q3 EPS guided to $19 at the midpoint vs. Street expectations of $11), questions arose about whether this marked peak strength. Five Below (FIVE) gained 3% after a solid beat and above-consensus Q1 guidance, with any weakness likely attributed to profit-taking.

Trading activity was subdued, with overall activity levels rated a 3 on a 1-10 scale. Asset managers were net sellers of $3 billion, driven by broad supply across all sectors, particularly in tech and financials. Hedge funds were net sellers of $1 billion, also focused on tech, macro, and discretionary sectors.

The FOMC maintained the target range for the fed funds rate at 3.5-3.75%, with only Governor Stephen Miran dissenting (contrary to Goldman Sachs’ prediction of three dissents). The Summary of Economic Projections (SEP) remained largely unchanged, predicting one rate cut each in 2026 and 2027, higher PCE inflation, and stronger GDP growth in the longer run. The median longer-run fed funds rate forecast edged up slightly to 3.125%, while the unemployment rate forecast for 2026 remained unchanged at 4.4%. Goldman Sachs revised its rate cut forecast to September and December (from June and September).

In derivatives, the Fed’s hawkish stance and negative geopolitical developments led to significant downside moves, with the market realizing over two straddles. Volatility was bid across the curve, particularly in the front end, with notable skew relaxation in the Nasdaq 100 (NDX). The VIX futures curve inverted again, following earlier declines in VIX expiry. Flows in fixed-strike options were quieter, with a tilt toward floating-strike convexity buyers as the S&P 500 hovered near its 200-day moving average. Dealer gamma positioning remains max short down 1%, which is unsupportive but not significantly impactful. Looking ahead, jobless claims data will be released tomorrow, followed by Quad Witching on Friday, with an implied market move of 1.52% through the end of the week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!